February 27th, 2026

Public

Germany B2B e-invoicing: An implementation overview

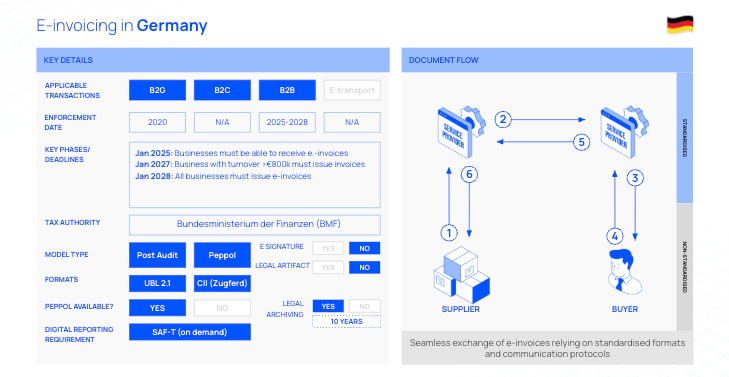

Germany is in the middle of a phased B2B e-invoicing rollout. Since 1 January 2025, businesses established in Germany must be able to receive and process structured electronic invoices for domestic B2B transactions.

Germany’s approach is currently focused on digitisation between trading partners, without mandatory, real-time invoice clearance by the tax authority. That said, requirements are expected to evolve over time as Germany aligns with EU ViDA and future digital reporting requirements ahead of the 1 July 2030 deadline.

Timeline for Germany

1 January 2025: All domestic businesses must be able to receive and process structured e-invoices (domestic B2B).

End of 2026: End of transition period for “other invoices” (for example paper and non-compliant PDFs).

1 January 2027: Domestic businesses with annual turnover over €800k must issue structured e-invoices.

1 January 2028: All domestic businesses must issue structured e-invoices.

What you must know about Germany

Scope and model: The mandate applies to domestic B2B transactions between German-established entities. Invoice exchange is decentralised (supplier and buyer model). There is no central B2B platform today.

Format requirements (EN 16931): Structured e-invoices must comply with EN 16931.

Common syntaxes: UBL, Peppol BIS and UN/CEFACT CII. xRechnung for B2G.

ZUGFeRD is also permitted (hybrid PDF/A-3 with embedded XML), provided it is EN 16931-compliant.

What changes in practice (2025–2026): Paper, PDFs, and other non-EN 16931 electronic formats are treated as “other invoices”. They are allowed during the transition, but will no longer be valid after 2026.

Transmission protocols: Recipients must provide an email inbox for receipt of e-invoices. Trading partners can agree alternative transmission methods such as Peppol, AS2, SFTP, or providing invoices for download via a customer portal.

Storage and audit readiness: E-invoices must be stored to ensure authenticity of origin, integrity of content, and legibility. In practice, organisations should plan for long-term archiving obligations (commonly 10 years).

Regulatory direction: The mandate was formalised through the Growth Opportunities Act, with additional clarification published by the German Federal Ministry of Finance (BMF) (draft guidance issued in 2024) on how e-invoices should be issued and handled.

How a managed compliance service helps

For large organisations, the main risk is not only meeting a single mandate, but maintaining a scalable approach across formats, protocols, partner variability, and ongoing regulatory change.

With ecosio’s managed compliance service for e-invoicing, we help teams:

Connect once via a single gateway to exchange e-invoices with customers, suppliers, and networks.

Keep formats compliant through validation and conversion, including EN 16931-aligned handling.

Support multiple transmission options (email-based receipt, Peppol, AS2, SFTP, and more) based on each partner’s capability.

Stay future-ready as Germany’s model moves towards broader EU digital reporting expectations.

Want to know more about Germany? Have a deeper look into this country in our country profile page, our FAQ has been especially popular for answering common questions about this mandate. In case you’re ready to discuss how ecosio can help your specific business case for Germany and many other countries, get in touch today!

The ecosio Product Team